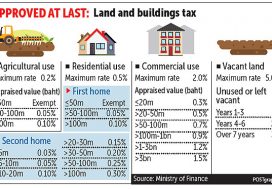

Several Thai government agencies have acted in concert to provide many taxpayers with an additional extension to the deadline for paying the 2020 land and building tax (LBT), and to clarify procedural matters for collecting the new tax, which is being instituted for the first time in 2020.

On August 27, 2020, the director of the Fiscal Policy Office and spokesperson of the Ministry of Finance issued an explanatory announcement about the collection of the LBT for 2020, reassuring owners of land or buildings over concerns that they would be charged a fine (of up to 40% of the outstanding tax payment) or surcharge (equal to 1% of the outstanding payment per month) for not paying LBT by the deadline at the end of August 2020. Specifically, the announcement confirmed that owners would not be charged if they either had not received the LBT assessment form, or if the property subject to LBT is covered by an extension or postponement of the tax payment deadline announced by the Bangkok Metropolitan Administration (BMA) or, for properties outside Bangkok, the relevant municipality or local administrative office.

Supporting that announcement, the BMA and many other administrative offices around the country have officially extended the payment deadline. The BMA’s announcement, issued on August 28, 2020, set a new payment deadline of October 31, 2020, and confirmed that owners would not be subject to fines or surcharges if they pay the LBT by that date.

To limit any risk of surcharges, owners of land or buildings who have not received the LBT assessment form are advised to check with the relevant district office in Bangkok, or municipality or local administrative office where the property is located, to ascertain whether the form has been sent. Those outside Bangkok should also check whether any extension or postponement of the tax payment deadlines has been granted.

As for what property owners can expect under normal circumstances in future years, the Land and Building Tax Act B.E. 2562 (2019) stipulates that the LBT assessment form will be sent to the owners of land or buildings on an annual basis. If the assessment is correct, the owners may pay the LBT at a district office (for property in Bangkok), a municipality or local administrative office (for property elsewhere), or via other methods prescribed by authorities (e.g., banking counters, mobile banking via QR code, online banking etc.). Owners may contest LBT tax assessments by submitting an appeal or objection within 30 days of receipt of the LBT assessment form.

Source: Tilleke & Gibbins